Table of Contents

Introduction

Imagine finally reaching your retirement years, only to realize your savings aren't enough to cover your basic needs. This is a stressful reality for many, but it's a situation you can avoid with a solid retirement planner. Planning for retirement can feel overwhelming with so many variables—from future inflation and healthcare costs to understanding complex financial accounts. Where do you even begin?

This comprehensive guide is your starting point. We'll break down the essentials of effective retirement planning, covering everything from calculating your needs to navigating key accounts like Roth IRAs and understanding Required Minimum Distributions (RMDs). Whether you're just starting your career or are a few years from retirement, this article will equip you with the knowledge to build a secure financial future.

By the end, you'll have a clear action plan and the tools to estimate your retirement needs confidently.

Quick Answer Section

A retirement planner is a comprehensive strategy, not just a single tool, used to estimate the income and savings needed for a comfortable retirement. It involves calculating future expenses, projecting income from sources like Social Security and investments, and using tools like a retirement calculator to assess if you're on track. An effective planner helps you make informed decisions about saving, investing, and withdrawing funds to ensure financial security throughout your post-work years.

What is a Retirement Planner?

At its core, a retirement planner is a comprehensive strategy and process for setting retirement income goals and the actions needed to achieve them. It's not merely a single retirement calculator; it's the entire framework. A retirement planner considers multiple facets of your financial life, from your current savings rate and investment portfolio to future income streams like Social Security, pensions, and part-time work.

Think of it as your financial roadmap for the decades after you stop working. A good retirement planner must be flexible enough to adjust for life changes, market fluctuations, and shifting goals. It's about ensuring you have enough money not just to survive, but to thrive during your retirement years, enjoying the lifestyle you envision.

Why a Retirement Planner Matters

Without a plan, you're essentially navigating your financial future in the dark. A retirement planner is crucial for several reasons. First, it provides a clear, realistic picture of your financial future, helping you understand the gap between where you are now and where you need to be. This awareness is the first step toward making meaningful changes.

Second, a comprehensive plan helps you identify potential shortfalls early. For instance, you might discover that you need to save more aggressively or adjust your investment strategy to meet your goals. It also helps you make informed decisions about major financial choices, such as when to claim Social Security benefits or how to manage withdrawals from different accounts to minimize taxes. Finally, having a well-thought-out plan provides immense peace of mind, reducing anxiety about your financial future and allowing you to enjoy your retirement years fully.

How a Retirement Planner Works

A retirement planner works by taking your current financial information, projecting it into the future, and comparing it against your estimated retirement needs. While the process can be complex, it can be broken down into five key steps. This gives you a clear framework to follow whether you're doing it manually or using a digital retirement planner tool.

Step-by-Step Breakdown

- Estimate Your Retirement Expenses: Start by calculating your current monthly expenses and predicting how they might change. Will your mortgage be paid off? Will travel costs increase? Don't forget healthcare and inflation.

- Project Your Income Sources: List all potential income streams for retirement, including Social Security, pensions, rental income, and part-time work. Use a social security calculator for more precise estimates.

- Calculate Your Retirement Needs: Determine the total amount of savings you'll need. Many experts suggest you'll need 70-80% of your pre-retirement income, but this varies.

- Assess Your Current Savings: Evaluate your current retirement savings across all accounts (401(k), IRA, Roth IRA, etc.). This is where a retirement calculator is most useful.

- Identify the Gap and Plan: Compare your projected income with your estimated expenses and savings. If there's a gap, adjust your savings rate, investment strategy, or retirement timeline.

Using a retirement planner tool can automate these calculations, allowing you to adjust variables like age, inflation, and savings rate to see different outcomes.

Quick Reference Table: Key Retirement Accounts & Distribution Rules

| Account Type | Contributions | Tax Treatment | RMD Age (2026) |

|---|---|---|---|

| Traditional 401(k)/IRA | Pre-tax | Taxed as ordinary income upon withdrawal | 73 (if born 1960 or later) |

| Roth 401(k)/IRA | After-tax | Tax-free growth and withdrawals (if rules met) | No RMD for Roth IRA, Roth 401(k) subject to RMD |

| SEP IRA | Pre-tax (employer contributions) | Taxed as ordinary income upon withdrawal | 73 (if born 1960 or later) |

Note: RMD rules are complex. Use a rmd calculator for specific guidance.

Step-by-Step Guide: Calculating Your Retirement Needs

The Manual Method

You can manually estimate your retirement needs using a formula. For example, if you estimate your annual expenses in retirement at $50,000, and you believe you can safely withdraw 4% of your portfolio each year, you would need $50,000 / 0.04 = $1,250,000 in savings. This method gives a simple starting point.

The Modern Method (Using a Retirement Calculator)

Using a retirement calculator is much more efficient and accurate. A retirement planner tool can handle complex calculations, including inflation, variable rates of return, and tax implications. You simply input your current age, income, savings, and desired retirement age. The tool then projects your savings growth, estimates your income needs, and shows you the probability of achieving your goal.

Best Practices

- Be Conservative: Use realistic assumptions for investment returns (e.g., 6-7% for stocks) and inflation (e.g., 3-4%).

- Factor in Healthcare: Healthcare costs are a significant expense; consider using an ira distribution calculator and healthcare cost estimators.

- Review Annually: Your retirement planner is a living document. Review and adjust it at least once a year or after any major life event.

Common Mistakes in Retirement Planning

Underestimating Healthcare Costs

A major misstep is failing to account for rising healthcare costs. Many retirees find that a significant portion of their budget goes towards health insurance premiums and out-of-pocket medical expenses.

Solution: Use a required minimum distribution calculator and healthcare-specific calculators to build a more accurate budget.

Forgetting About Required Minimum Distributions (RMDs)

Many people don't plan for RMDs. Starting at age 73, you are required to withdraw a minimum amount from most tax-deferred retirement accounts. Failing to do so results in a 25% penalty on the amount you should have withdrawn.

Solution: Plan ahead. An rmd calculator can help you estimate your required withdrawal and incorporate it into your tax strategy.

Claiming Social Security Too Early

Taking Social Security benefits at age 62 can permanently reduce your monthly benefit. While sometimes necessary, it's often a mistake if you can afford to wait until your full retirement age (67) or even age 70 to maximize your benefit.

Solution: Use a social security calculator to understand the long-term impact of your decision.

Real-World Use Cases

Here are a few scenarios where a retirement planner proves invaluable:

- Sarah, 30, Marketing Professional: Sarah uses a retirement planner to understand how much of her salary she needs to contribute to her 401(k) to retire by 65. She discovers she needs to increase her contribution to 15% to reach her goal.

- Mark, 50, Teacher: Mark uses the planner to simulate his retirement income, balancing his pension with withdrawals from his Traditional and Roth IRA. He uses a roth ira estimator to decide the best strategy to minimize taxes.

- Linda, 60, Small Business Owner: Linda wants to retire in 5 years but is worried about her savings. She uses a retirement calculator to understand her potential shortfall and decides to delay her retirement to 67 to bridge the gap.

- David, 72, Retired Engineer: David must take his RMD this year. He uses an rmd calculator to determine the exact amount and chooses to take a qualified charitable distribution (QCD) to reduce his taxable income.

- Amy, 55, Project Manager: Amy wants to estimate if she can afford to retire early. She uses a retirement planner to stress-test her portfolio against different scenarios and decides to consult a financial advisor.

- James, 40, Couple with Two Kids: James and his wife use a retirement planner to balance saving for college with their own retirement needs. They adjust their contributions to ensure they are on track for both goals.

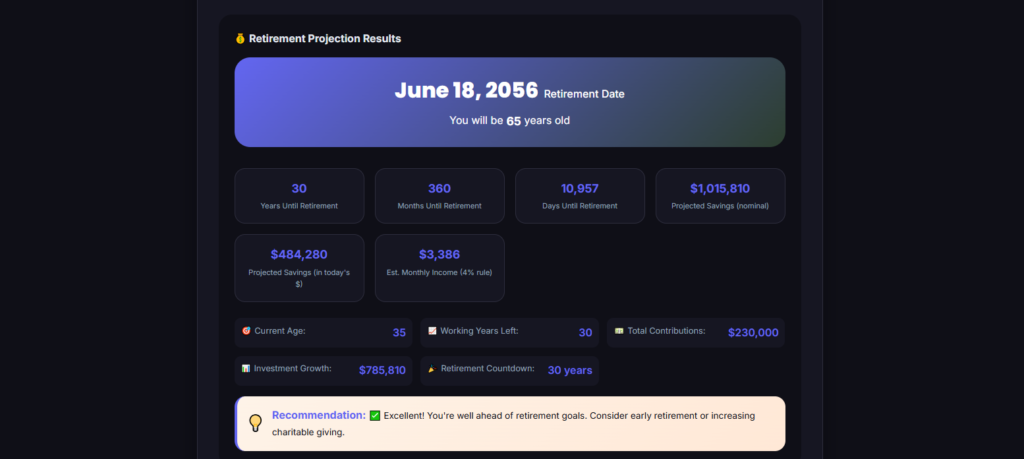

Simplify Your Planning with the MiniToolsPro Retirement Age Calculator

While understanding the principles of retirement planning is essential, manually calculating everything can be time-consuming and prone to error. Instead of building complex spreadsheets from scratch, you can use a specialized tool to get accurate results in seconds.

Our free Retirement Age Calculator is designed to take the guesswork out of your retirement planner strategy. Simply enter your birth date and a target date, and the tool instantly computes your exact age at that time. While primarily an age calculator, it serves as a crucial first step for any retirement plan, helping you pinpoint your target retirement date precisely.

Why Use Our Retirement Age Calculator?

- Instant & Accurate: Get your exact age down to the year, month, and day in milliseconds.

- Easy to Use: No complicated forms. Just input your birth date and the date you want to check.

- Time-Saver: Eliminate manual age calculations, especially when planning for key milestones like retirement age.

- Foundation for Bigger Plans: Use this precise age calculation as a foundation for more complex retirement calculator models and financial plans.

Accurate age determination is a critical component of any retirement planner.

Advanced Tips & Best Practices

- Don't Forget Inflation: When using a retirement planner, adjust for inflation. A dollar today will be worth less 20 or 30 years from now. Use a tool that factors in a realistic inflation rate (e.g., 3%).

- Asset Allocation Matters: Your investment mix should evolve as you approach retirement. A younger person can afford more risk (stocks), while someone nearing retirement should shift toward bonds.

- Consider Tax Efficiency: Think about where you hold your assets. Are you using a Roth IRA? What is your strategy for a roth account calculator? Understanding the tax implications of your accounts is key.

- Plan for the Longevity: The risk of outliving your savings is real. Plan for a retirement that could last 30 years or more.

Frequently Asked Questions (FAQ)

What is a retirement planner and how does it work?

A retirement planner is a tool or strategy that helps you project your future finances by analyzing your current savings, expected returns, and retirement goals. It works by collecting your data and running simulations to forecast your financial standing at different points in the future.

Can a retirement calculator help me with Roth IRA planning?

Yes, many advanced retirement planner tools include a roth ira estimator to help you see how Roth contributions affect your long-term after-tax income. They are invaluable for comparing Roth vs. Traditional account strategies.

What is the difference between a retirement calculator and a retirement planner?

A retirement calculator is a tool used to crunch numbers, while a retirement planner is the overarching strategy. The planner uses data from the retirement calculator to create a full financial action plan.

How do I use an RMD calculator?

To use an rmd calculator, you typically input your age, the balance in your tax-deferred retirement accounts (like a Traditional IRA), and your life expectancy factor. The calculator will then provide the minimum amount you must withdraw for that year.

What age do I have to start taking RMDs?

For individuals born in 1960 or later, the age to begin taking RMDs is 73. Use a required minimum distribution calculator for precise figures and potential future changes.

Are Roth IRA withdrawals subject to RMD?

No, Roth IRAs are not subject to RMDs during the owner's lifetime. This is a key advantage for estate planning. However, a roth account calculator can help you assess the best conversion strategy.

What is a safe withdrawal rate for retirement?

A common rule of thumb is the 4% rule. This suggests you can withdraw 4% of your savings in the first year of retirement and adjust for inflation thereafter. However, many experts now suggest a more dynamic approach, especially if using a retirement planner with Monte Carlo simulations.

Is Social Security enough for retirement?

No, Social Security is generally designed to replace only about 40% of your pre-retirement income. You'll need additional savings and a retirement planner to generate the rest. A social security calculator can show you your estimated benefits.

How much of my income do I need to save for retirement?

Many financial experts recommend saving 15% to 20% of your gross income annually for retirement. However, this percentage depends on when you start, your target retirement age, and the lifestyle you want. A good retirement calculator can provide a more personalized answer.

Can I use a retirement planner if I'm self-employed?

Absolutely. In fact, it's even more critical. A retirement planner can help you navigate SEP IRAs, Solo 401(k)s, and fluctuating income, ensuring you stay on track without an employer-provided plan.

Final Thoughts

Creating a secure retirement doesn't happen by accident. It requires a thoughtful, proactive approach. While the process may seem daunting, breaking it down into manageable steps is the key. By understanding your needs, projecting your income, and using reliable tools like the retirement planner concepts discussed here, you're taking a powerful and proactive step toward financial freedom.

Don't wait until it's too late. Start today, even if it's just by assessing your current situation. The journey of a thousand miles begins with a single step, and your journey to a comfortable, worry-free retirement starts now. Use the tools and knowledge available to you, including the Retirement Age Calculator, to set a solid foundation for your future.

Related Tools You May Find Useful

- Compound Interest Calculator – Visualize the power of compound interest on your savings and investments.

- Percentage Calculator – Easily calculate percentages, useful for understanding tax rates or savings goals.

- Discount Calculator – Useful for understanding sale prices and saving strategies.

- Random Number Generator – A handy tool for simulating various scenarios or random financial projections.

- Typing Speed Test – Take a fun and useful break to test your typing speed!

- Word Counter – Keep track of the word count in your financial documents or reports.

Share this article 👇

![Date to Date Calculator]](https://minitoolspro.com/blog/wp-content/uploads/2026/06/Date-to-Date-Calculator.jpg)

0 Comments